Open Finance

Screen Scraping Vs. Open Banking

Unbar the complexities of screen scraping versus Open Banking with Fiskil's comprehensive analysis. Gain insights into their respective roles, challenges.

A while back, a report from the UK's Competition and Markets Authority was published on banking. The report showed that older, more established banks in today’s society do not have the obligation to compete for new customers while newer, smaller banks struggle to access the market and grow. As a result, customers aren’t given enough choice when it comes to banking services, and control over their money or financial data.

Australia’s Royal Commission into the banking sector reinforced this notion that consumers are getting a bad deal.

The good news is that the inevitable evolution of technology, particularly in financial services, is favourable for the customer. Open banking is one of these evolutions, and is a direct response to an outdated method for retaining data, screen scraping. Let’s have a look at the advantages and disadvantages of both.

What is Screen Scraping?

Businesses that use screen scraping for their services fetch the customer’s data when, more often than not, the users haven’t given consent to. How this works is through a third-party service. It asks for access to your credentials along with your unique bank account codes. With that information, the third-party service can impersonate you when they contact your bank account online so they can access your account on your behalf and retrieve all of your data. It should be noted that the handing out of your internet banking details is against most banks' T’s & C’s.

For developers, the benefit with screen scraping comes from the lack of barriers and the lack of an expiry date for accessing the data, meaning there is ongoing access to your account and an omission of the standard security regulations the bank has in place. The disadvantage is that through screen scraping you are not in an agreement with the bank to receive reliable data, if the bank changes the website that is being scraped the software algorithm will fail and require changing.

As an example, let’s say you want to get a home loan through a particular lender. The lender will need to check your affordability as they usually do. Then a third-party provider asks for your bank access details and credentials to contact your bank pretending to be you and retrieve the information required. During this process, the third-party provider gains access to all the data on your bank account, such as salary, your previous shopping transactions, your current balance, savings, contacts, and more. There is also no restriction on storing this information, again giving the consumer the worst deal.

What is Open Banking?

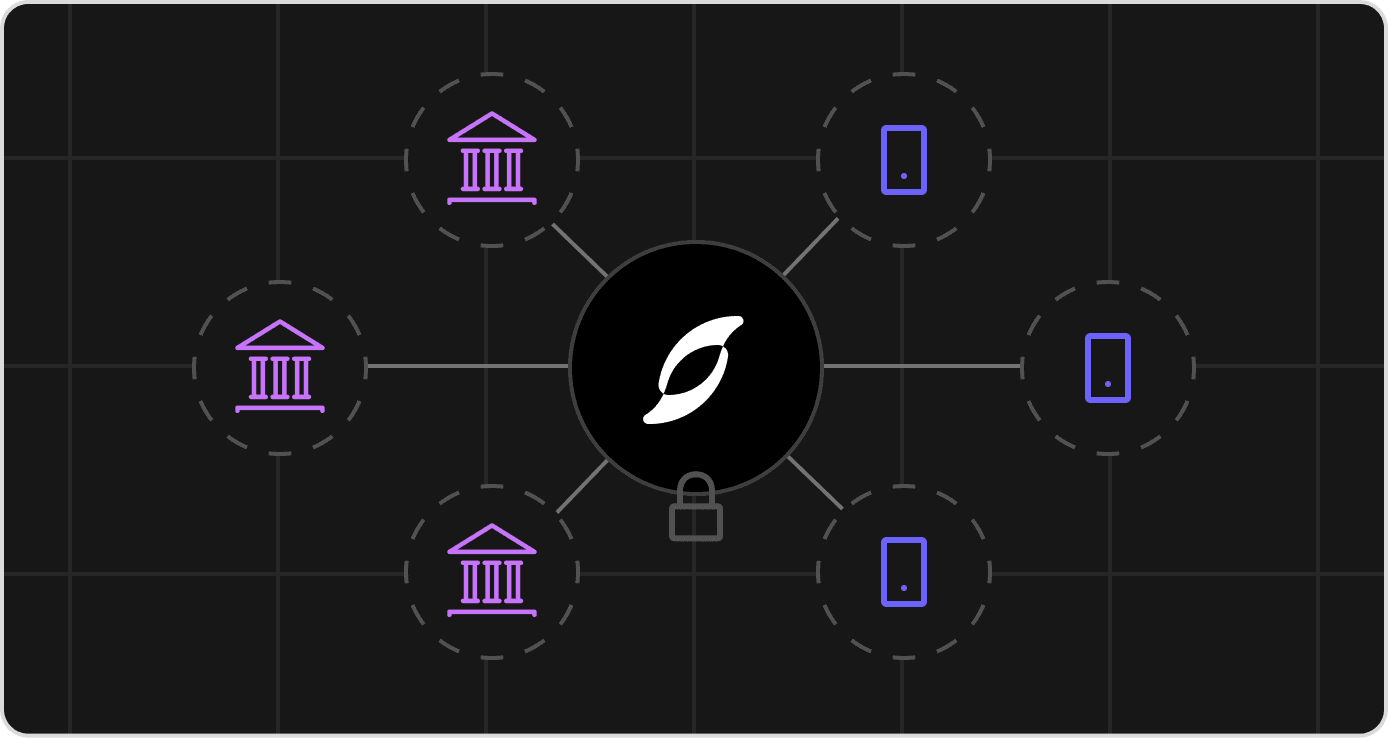

Open banking, on the other hand, enables you to give consent to those third-party providers that will analyse your data for you, but in a secure way. It is built on secure Application Programming Interfaces (APIs) that come from verified Data Holder institutions. The third-party providers access data reliably with a limited expiry date, unlike with screen scraping, where they have unlimited access to your bank account.

This way, the consumer is always in control of their transactions and what data is shared. Open banking also gives you the ability to stop access to your data at any time.

An example of open banking and how it accesses your banking data would be an app with a regulated third-party provider that uses open banking. When you want to use an app like this for online purchases or money management, it asks you if it can access your account and transaction data safely. If you consent to this, you are redirected to your bank’s website, where you log in with one-time credentials - like a phone number and verification code. This way, the need to allow never-ending access to internet banking details is completely eliminated, and a much cleaner user experience is provided. Your login details stay safely on the bank’s website and are never shared with the open banking app. Instead of giving your credentials to a third-party provider that can access your complete data at any time, open banking asks for you to choose what you want to share. You can also select precisely for how long the access will be valid so that you are in complete control over your data sharing.

Bottom Line

All in all, when comparing both systems, there is no doubt that open banking has numerous benefits with tangible financial impacts. Complete control over personal data, better money management, improved security, and overall a unique customer experience. As such, this type of innovative banking provides satisfaction and digital agility in a way screen scraping can’t. When businesses use open banking for their services, they show increased customer lifetime value.