Open Finance

Guide to becoming accredited to use open banking in Australia

Open the process of becoming accredited to use Open Banking in Australia with Fiskil's vast guide. Gain insights into requirements, application procedures.

Why use Open Banking?

In the past decade, Australia’s finance sector has been dominated by the Big 4 banks. The paramountcy of the Big 4 banks has traditionally made it difficult for smaller players such as Fintech start-ups to shake up the finance sector - that is, until the advent of the Consumer Data Right (CDR).

The CDR, introduced in February 2020, is changing the world of finance. The CDR gives Australian consumers the right to direct the information they already share with institutions to be safely shared with others they trust. Businesses can use CDR to provide personalised services and experiences for their customers by using open banking data to gain insights into what customers want. Third party financial service providers are able to leverage open banking data not only to personalise their target consumer market, but also to develop new and innovative solutions that will put them ahead of competitors.

Sounds great - so how do I become accredited?

If your business wants to participate in Australia’s open banking data scheme, it will need to become accredited or work with intermediaries who are.

Under the CDR rules, all businesses requesting access to CDR data must be accredited or have access to a party that has been accredited by the Australian Competition and Consumer Commission (ACCC). The ACCC has recently released updated guidelines on the CDR accreditation process to reflect the latest CDR rules.

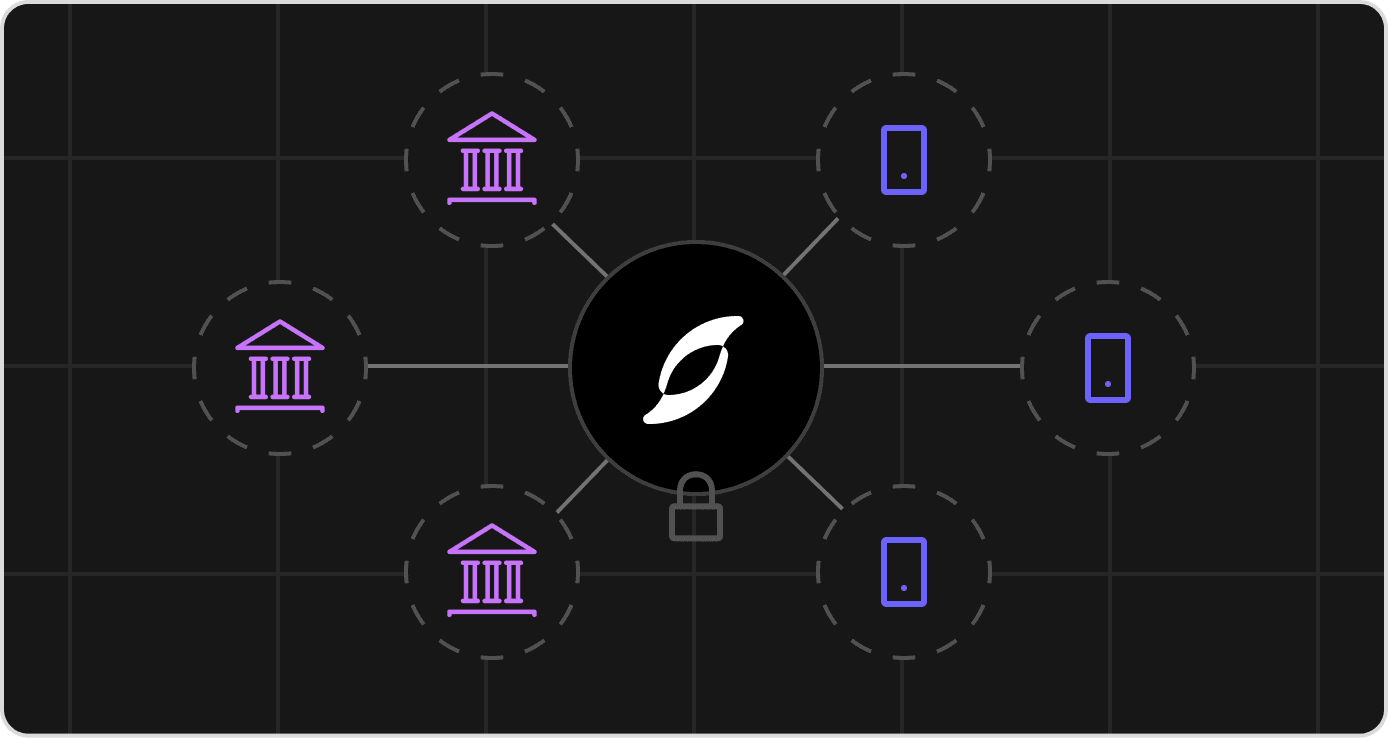

These companies are called Accredited Data Recipients (ADRs). Banks and other Authorised Depository Institutions (ADIs) such as credit unions are called Data Holders. ADRs access consumer data by connecting their APIs (application programming interfaces – the software that connects your system to others) to those owned by Data Holders.

There are various ways to access open banking data, not all of which require accreditation. The different pathways to gaining access to CDR data are summarised below.

| Pathway | Description | Accreditation required? | Data collection allowed? |

|---|---|---|---|

| Unrestricted accreditation | Gaining unrestricted accreditation is the highest level of accreditation. This means that your business can become an ADR itself. Businesses at the unrestricted level can act as a sponsor to an affiliate and engage a CDR representative/outsourced service provider. | Yes | Yes |

| Sponsored Accreditation | Businesses with sponsored accreditation: a) Must have a sponsor to collect CDR data/provide goods or services to CDR consumers b) Must only collect CDR data through sponsor/other accredited person/sponsor’s outsourced service provider c) must not engage an outsourced service provider to collect data or engage a CDR representative | Yes. However, applicants are able to self-assess and attest to information security requirements | Not directly from data holders but may request its sponsor collect data from the data holder and pass it on |

| CDR representative model | Provides an ‘agency-like’ model that allows unaccredited persons (CDR representative) to partner with an unrestricted accredited person (the principal) to provide goods and services using CDR data. A CDR representative may only have one principal. | No | No |

Accreditation will look different depending on which pathway you choose. The CDR pathway that you choose for your business depends on the use case or cases that are the best fit for your customers’ needs.

Becoming an ADR

If your business wants to become an ADR, it will need to gain accreditation through the CDR Participant Portal . Obtaining ADR accreditation can be a lengthy process and can take as long as 4-6 months. You can refer to the step-by-step guide on the ACCC CDR page to get started.

Being sponsored by an open banking ADR

Under this type of arrangement you need to be accredited as a Sponsor by the ACCC and enter a sponsorship arrangement with an unrestricted ADR, such as Fiskil. This pathway will reduce the costs of accreditation, which can be a barrier to entry for many businesses.

As a Sponsor ADR, Fiskill can assist by: Connecting to Data Holder APIs; Collecting all open banking data from customers on your behalf; Handling the consent requirements; and Ensuring compliance with the CDR rules.

Becoming a CDR representative of an ADR

The CDR representative model means that accreditation is not required, but there are limits on what kind of products or services you can offer. Under this model, an unrestricted ADR can appoint you as their representative and act as your intermediary, and be responsible for collecting all open banking data that you will use to provide goods and services to your customers. The unrestricted ADR takes charge of all things compliance, data consent and collection.

How can Fiskil help?

Fiskil handles the hard work when it comes to Open Banking and the CDR so that companies can focus on their core business. Fiskil APIs will instantly connect your application or website to your users’ bank accounts to provide a more streamlined, personalised experience. To find out more about how Fiskil can help enhance the user experience for your customers, get in touch!